Smarter mobile money through big data analytics

Approximately 2.5 quintillion bytes, or 2.3 trillion gigabytes, of data is generated every day around the world. The full potential of all this information is yet to be discovered with estimates that only 0.5% undergoes analysis, while one in three business leaders make decisions based on insufficient data.

The volume of data available to service providers today is an enormous resource for better understanding the customer base. Data analytics helps overcome potential issues, promotes faster adoption of new services and increases transactions.

Big data and mobile money

The mobile service providers access to big data offers a huge advantage over formal financial institutions, who cannot easily tap into their clients daily life. In defining patterns, trends and links occurring over time, the mobile money ecosystem can unlock hidden value, such as fraud management and credit scoring for financial services.

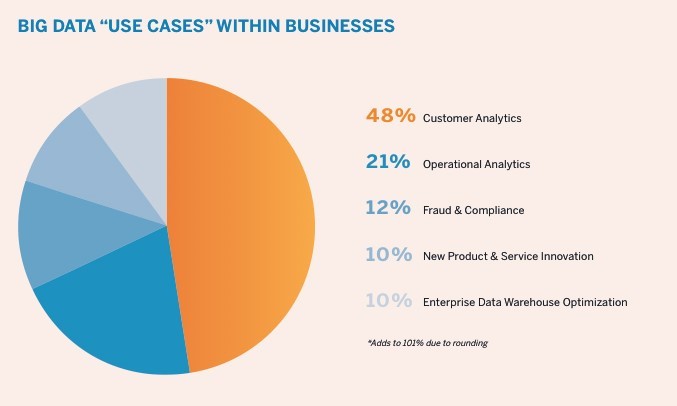

Graph: How is big data used?

Fraud management

Suspicious behaviour manifests in different ways. Big data analytics link heterogeneous information from transaction data, which enables the service provider to pick up on this behaviour. For example, a series of cash-in transactions to the same account, from different locations, might be an attempt to avoid paying for domestic transfers, or several cash-ins immediately followed by a cash-out could indicate money laundering. There are two methods of reporting for suspicious behaviour. The first is system generated in real time upon anomaly detection, which is then approved or rejected by the fraud analyst. The second requires the fraud analyst to generate a daily report for post-analysis. Best practice states that no actions are purely automated, the fraud analyst always has the final say. This prevents unjustified automatic rejection cases.

Machine learning further complements fraud management processes. In using the past to predict the future, fraud analysts define detection parameters based on normal behavioural patterns from transaction history. As a populations behaviour evolves over time, the parameters must adapt to remain optimal. In response to this, machine learning predicts a natural evolution of behaviour based on historical data as well as previous actions taken by fraud managers in decision making. It then proposes modifications to the detection model for future anomaly detection.

Credit scoring

Limited access to financial services in emerging countries means that some people arent able to generate a financial diary to produce a credit score. This is problematic for a lender needing to rate an individuals loan repayment capacity. Big data supports credit scoring technology for mobile financial services through in-depth analysis of a subscribers records. Here, credit scoring is employed in two ways.

- A subscriber wants to receive a loan. Once approached, the agent uses transaction data to decide whether to accept or decline the request.

- A service provider wants to offer a credit lending service to a broad section of society. The populations data is scanned, and categorised according to a given credit score used to evaluate the viability of offering this service to certain categories.

For example, a local farmer needs to invest in crop fertiliser to increase his income, but has insufficient funds to make the purchase. The service provider identifies this common problem as an opportunity to provide a mobile loan service tied to the provision of a product. Before targeting farmers for a new campaign, the service provider uses credit scoring analytics extracted from several sources to determine lending eligibility.

Firstly, the service provider looks at their own data for indicators of trustworthiness, starting with a subscribers mobile money transactions and electronic recharge records as these may demonstrate behavioural similarities to a bank account. A responsible borrower may keep their phone topped up to a minimum threshold so they have credit in case of emergency. They may also search information previously provided to comply with customer due diligence. Know Your Customer (KYC) details a subscribers age range, noteworthy as those between 30-50 years old are considered mature and healthy enough for responsible lending. When this information is not available, the service provider can obtain additional data from third parties such as financial institutions to complete a thorough assessment.

About eServGlobal

eServGlobal offers mobile money solutions which put feature-rich services at the fingertips of users worldwide, covering the full spectrum of mobile financial services, consulting, mobile wallet, recharge, promotions and agent management. In addition, eServGlobals Apeiron tool facilitates data analytics and machine learning for business and liquidity management, including fraud management and credit scoring. For more information please go to eservglobal.com to organise a meeting at Africa Com in hall 4, stand 4G.

If you are interested in the opportunities for big data in Africa why not attend AfricaCom 2016? AfricaCom has a dedicated big data stream looking at data analytics, how data can spur better customer insights and financial inclusion, as well as how data can continue to build Africa's digital future. Find out what's on the agenda here.

Africa's biggest tech and telco event is taking place between the 14th - 18th November at the Cape Town ICC, find out more here.

You can sign up for a free visitor pass to the event here.

You can book your silver, gold and platinum AfricaCom tickets to all sessions here.

Be part of the African tech and telco conversation, here:

Approximately 2.5 quintillion bytes, or 2.3 trillion gigabytes, of data is generated every day around the world. The full potential of all this information is yet to be discovered with estimates that only 0.5% undergoes analysis, while one in three business leaders make decisions based on insufficient data.

The volume of data available to service providers today is an enormous resource for better understanding the customer base. Data analytics helps overcome potential issues, promotes faster adoption of new services and increases transactions.

Big data and mobile money

The mobile service providers access to big data offers a huge advantage over formal financial institutions, who cannot easily tap into their clients daily life. In defining patterns, trends and links occurring over time, the mobile money ecosystem can unlock hidden value, such as fraud management and credit scoring for financial services.

Graph: How is big data used?

Fraud management

Suspicious behaviour manifests in different ways. Big data analytics link heterogeneous information from transaction data, which enables the service provider to pick up on this behaviour. For example, a series of cash-in transactions to the same account, from different locations, might be an attempt to avoid paying for domestic transfers, or several cash-ins immediately followed by a cash-out could indicate money laundering. There are two methods of reporting for suspicious behaviour. The first is system generated in real time upon anomaly detection, which is then approved or rejected by the fraud analyst. The second requires the fraud analyst to generate a daily report for post-analysis. Best practice states that no actions are purely automated, the fraud analyst always has the final say. This prevents unjustified automatic rejection cases.

Machine learning further complements fraud management processes. In using the past to predict the future, fraud analysts define detection parameters based on normal behavioural patterns from transaction history. As a populations behaviour evolves over time, the parameters must adapt to remain optimal. In response to this, machine learning predicts a natural evolution of behaviour based on historical data as well as previous actions taken by fraud managers in decision making. It then proposes modifications to the detection model for future anomaly detection.

Credit scoring

Limited access to financial services in emerging countries means that some people arent able to generate a financial diary to produce a credit score. This is problematic for a lender needing to rate an individuals loan repayment capacity. Big data supports credit scoring technology for mobile financial services through in-depth analysis of a subscribers records. Here, credit scoring is employed in two ways.

- A subscriber wants to receive a loan. Once approached, the agent uses transaction data to decide whether to accept or decline the request.

- A service provider wants to offer a credit lending service to a broad section of society. The populations data is scanned, and categorised according to a given credit score used to evaluate the viability of offering this service to certain categories.

For example, a local farmer needs to invest in crop fertiliser to increase his income, but has insufficient funds to make the purchase. The service provider identifies this common problem as an opportunity to provide a mobile loan service tied to the provision of a product. Before targeting farmers for a new campaign, the service provider uses credit scoring analytics extracted from several sources to determine lending eligibility.

Firstly, the service provider looks at their own data for indicators of trustworthiness, starting with a subscribers mobile money transactions and electronic recharge records as these may demonstrate behavioural similarities to a bank account. A responsible borrower may keep their phone topped up to a minimum threshold so they have credit in case of emergency. They may also search information previously provided to comply with customer due diligence. Know Your Customer (KYC) details a subscribers age range, noteworthy as those between 30-50 years old are considered mature and healthy enough for responsible lending. When this information is not available, the service provider can obtain additional data from third parties such as financial institutions to complete a thorough assessment.

About eServGlobal

eServGlobal offers mobile money solutions which put feature-rich services at the fingertips of users worldwide, covering the full spectrum of mobile financial services, consulting, mobile wallet, recharge, promotions and agent management. In addition, eServGlobals Apeiron tool facilitates data analytics and machine learning for business and liquidity management, including fraud management and credit scoring. For more information please go to eservglobal.com to organise a meeting at Africa Com in hall 4, stand 4G.

If you are interested in the opportunities for big data in Africa why not attend AfricaCom 2016? AfricaCom has a dedicated big data stream looking at data analytics, how data can spur better customer insights and financial inclusion, as well as how data can continue to build Africa's digital future. Find out what's on the agenda here.

Africa's biggest tech and telco event is taking place between the 14th - 18th November at the Cape Town ICC, find out more here.

You can sign up for a free visitor pass to the event here.

You can book your silver, gold and platinum AfricaCom tickets to all sessions here.

Be part of the African tech and telco conversation, here: